Content

Also, I read that occasionally, the old inventory that has been “on the books” for a long time at a very undervalued cost can be “sold off” and generate a profit spike . If you look at the calculations above, you will notice that instead of going from calculating the cost from week one, we instead started with the most recent week and worked backward. If you pay close attention, you also will notice that when we get to week three, we only sold 700 from the 900 produced that week.

An example of this is when a restaurant stocks up on canned food but continues to purchase fresh Why LIFO Is Banned Under IFRS ingredients. Rather than using the older canned goods, the staff use newer inventory instead.

The essential guide to restaurant inventory costing: all 3 techniques explained

For this reason, if LIFO is applied on a perpetual basis during the period, special inventory adjustments are sometimes necessary at year-end to take full advantage of using LIFO for tax purposes. Accurate inventory costing is a necessary evil in the restaurant industry.

This week our partners at Marketman have written a guide to inventory costing, one of the most challenging aspects of managing stock within a restaurant. Read on to learn all about the different methods you can use as well as how Marketman can help. It is not applicable in the United Kingdom, where stock valuation is typically recorded by either the average cost or FIFO valuation method. If the totals of the assets sold totals more than what was paid for them, then this is considered a capital gain and can be taxable.

Meet the IFRS team

I can’t buy and eat more, or pour gas on the ground just because it is cheap. Similarly, no one can make money raising prices, because I would have to spend less. It is a completely mysterious and stupid concept, divorced from any knowledge of reality. Stack Exchange network consists of 181 Q&A communities including Stack Overflow, the largest, most trusted online community for developers to learn, share their knowledge, and build their careers.

Is LIFO acceptable under GAAP?

It is acceptable if it is used for both International Financial Reporting Standards and the financial reporting standards of the individual country.

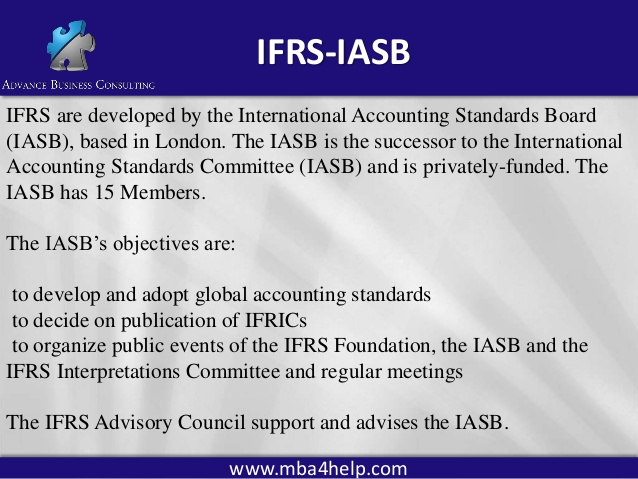

WAC is most appropriate for retailers who are selling a large number of identical or very similar items. Higher costs to a business mean a lower net income, which results in lower taxes. A global set of accounting standards was pioneered by the International Accounting Standards Committee, which was set up in 1973. Its successor the International Accounting Standards Board developed the International Financial Reporting Standards, the IFRS, used by publicly accountable companies. About 87% of jurisdictions in the world require the use of IFRS standards. The IASB was established in 2001 and has stakeholders from around the world. IFRS is balance sheet oriented and, on this basis, disallows LIFO as an inventory method.

Why would a company use FIFO instead of LIFO?

Conversely, if the LIFO assets are sold for less than the price they were purchased for, this would be considered a capital loss. LIFO is the opposite of the FIFO valuation method, which conversely assumes that the oldest recorded cost of units in stock are those being sold first and should be recorded as such. Under the LIFO method of stock management a company assumes that the newest units in stock are the ones being sold first – regardless of which units are actually sold first and are recorded appropriately in the books. The FIFO method is the more common and trusted method compared to LIFO, since it offers few discrepancies when calculating inventory’s value. However, LIFO is sometimes used when businesses are prone to higher COGS and lower profit margins. To make the best decision for your business, it’s important to consult your CPA. However, for accounting purposes, as long as you remove COGS from the last inventory replenishment cycle under LIFO, it doesn’t matter if you sell the oldest or latest inventory items first.

- Like IAS 2, transport costs necessary to bring purchased inventory to its present location or condition form part of the cost of inventory.

- Instead of the normal profit margin of $0.15 per gallon or $1,500 for ten thousand gallons, the company reports a gross profit of $2.28 per gallon ($2.70 sales price minus $0.42 cost of goods sold).

- FIFO will have a higher ending inventory value and lower cost of goods sold compared to LIFO in a period of rising prices.

- Next, whether acting in an external or an internal role, the CPA should help each U.S. firm understand how, or if, it would be affected by the elimination of LIFO for tax purposes.

- Note that you can also determine the cost of goods sold for the year by recording the value of each item sold.

An entity makes retrospective application only for the direct effects of the change . However, indirect effects—for example, bonuses—are reflected prospectively . Therefore, it will provide lower-quality information on the balance sheet compared to other inventory valuation methods as the cost of the older snowmobile is an outdated cost compared to current snowmobile costs. The main reason for excluding the LIFO is because IFRSs shifted its focus on balance sheet instead of income statement which is also known as balance sheet approach.

31 FASB, SFAC 2, “Qualitative Characteristics of Accounting Information” . See also FASB’s mission statement for discussion of the precepts followed in standard setting, /facts/index.shtml#mission. 4 Sec. 472 provides the authorization for the LIFO method, and the LIFO conformity requirement is articulated in Sec. 472. That Congress may be compelled to save LIFO would seem to run counter to recent behavior in both the House and the Senate. There have been several recent congressional attempts to repeal LIFO, but none of these received serious consideration.

If he sold another 2,000 cups, we would start calculating costs from week three, except now it will be 200 cups produced in week three. Let us take a look at a more comprehensive example of the calculation COGS using the LIFO method. Tommy owns a face cream production company and below is the account of his face cream production https://business-accounting.net/ cost in the last six weeks. As will be seen in the next chapter, similar arguments are made in connection with property and equipment—the reported amount and the value can vary greatly. However, those assets are not normally held for resale purpose so that current worth is of much less interest to decision makers.

WAC (Weighted Average Cost Method)

The LIFO method is an acronym used in accounting and many computational concepts for Last-In, First-Out. In accounting, this is used to compute the number of goods sold over a duration of time when taking inventory.

FIFO vs. LIFO Inventory Valuation – Accounting – Investopedia

FIFO vs. LIFO Inventory Valuation – Accounting.

Posted: Sat, 25 Mar 2017 14:01:00 GMT [source]